Abstract

This work extends the contagion model introduced by Nier et al. (J Econ Dyn Control 31(6):2033–2060, 2007. http://www.bankofengland.co.uk/publications/workingpapers/wp346.pdf) to inhomogeneous networks. We preserve the convenient description of a financial system using a sparsely parameterized random graph, but add several relevant inhomogeneities. These include well-connected banks, financial institutions with disproportionately large interbank assets, and big banks that focus on wholesale and retail customers. These extensions significantly enhance the model’s generality as they reflect realistic inhomogeneities that have a potentially decisive impact on a system’s stability. We find that large and well-connected banks have a surprisingly modest impact. However, institutions with disproportionately large interbank assets significantly increase the risk of contagion in networks. Moreover, these effects can be partly compensated by a redistribution of equity capital, even without increasing the total amount. However, the level of regulatory capital should be defined according to the interbank market position of a bank, and not the size of the bank.

Similar content being viewed by others

Notes

See Upper (2011) for a detailed discussion of these modeling assumptions.

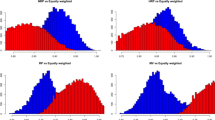

This effect can be understood if one recalls the model’s balance sheet construction rules and especially condition (4), which first settles imbalances in the interbank positions with external assets before distributing the remaining amount randomly. Hence, only this remaining amount is the subject of the inhomogeneous distribution enabled by \(\sigma _{E}\). As riskiness leads to banks with disproportionately large interbank assets, a bigger fraction of the external assets E is already assigned, owing to condition (4).

Note that the model construction does not take advantage of a constant percentage of net worth to total assets. Thus, the previous model construction is not affected by this model extension.

References

Aikman, D., Alessandri, P., Eklund, B., Gai, P., Kapadia, S., Martin, E., et al. (2009). Funding liquidity risk in a quantitative model of systemic stability. Bank of England Working Paper 372.

Allen, F., & Babus, A. (2009). Networks in finance. In P. Kleindorfer, J. Wind, & R. E. Gunther (Eds.), The network challenge. Upper Saddle River: Wharton School Publishing.

Allen, F., & Gale, D. (2000). Financial contagion. Journal of Political Economy, 108(1), 1–33.

Anand, K., Gai, P., Kapadia, S., Brennan, S., & Willison, M. (2012). A network model of financial system resilience. Bank of England Working Paper No. 458.

Berman, P., DasGupta, B., Kaligounder, L., & Kerpinski, M. (2011). On vulnerability of banking networks. arXiv:1110.3546v2 [q-finRM]

Blum, M., & Krahnen, J. P. (2014). Systemic risk in an interconnected banking system with endogenous asset markets. Journal of Financial Stability, 13, 75–94.

Caccioli, F., Catanach, T. A., & Farmer, J. D. (2012). Heterogeneity, correlations and financial contagion. Advances in Complex Systems, 15(supp02), 1250058.

Cifuentes, R., Ferrucci, G., & Shin, H. S. (2005). Liquidity risk and contagion. Journal of the European Economic Association, 3(2/3), 556–566.

Cihák, M., Muñoz, S., & Scuzzarella, R. (2011). The bright and the dark side of cross-border banking linkages. IMF Working Papers WP/11/186.

Cont, R., Moussa, A., & Santos, E. B. (2012). Network structure and systemic risk in banking systems. Working Paper Columbia Center for Financial Engineering.

Cont, R., Moussa, A., & Santos, E. B. (2013). Network structure and systemic risk in banking systems. In J. Fouque & J. Langsam (Eds.), Handbook of systemic risk (pp. 327–368). Cambridge: Cambridge University Press.

Eisenberg, L., & Noe, T. H. (2001). Systemic risk in financial systems. Management Science, 47(2), 236–249.

Elliott, M., Golub, B., & Jackson, M. O. (2014). Financial networks and contagion. American Economic Review, 104(10), 3115–3153.

Elsinger, H., Lehar, A., & Summer, M. (2006). Risk assessment for banking systems. Management Science, 52(9), 1301–1314.

Erdös, P., & Rényi, A. (1959). On random graphs, I. Publicationes Mathematicae (Debrecen), 6, 290–297. http://www.renyi.hu/~p_erdos/Erdos.html#1959-11.

European Central Bank. (2010a). Analytical models and tools for the identification and assessment of systemic risks. Financial Stability Review, 38–46.

European Central Bank. (2010b). Financial networks and financial stability. Financial Stability Review, 155–160.

Freixas, X., Parigi, B. M., & Rochet, J. C. (2000). Systemic risk, interbank relations, and liquidity provision by the central bank. In Proceedings (pp. 611–640). http://ideas.repec.org/a/fip/fedcpr/y2000p611-640.html.

Gai, P., & Kapadia, S. (2010). Contagion in financial networks. Proceedings of the Royal Society A, 466(2120), 2401–2423.

Georg, C. P. (2013). The effect of the interbank network structure on contagion and financial stability. Journal of Banking and Finance, 37, 2216–2228.

Hale, G. (2012). Bank relationships, business cycles, and financial crises. Journal of International Economics, 117, 196–215. http://www.frbsf.org/publications/economics/papers/2011/wp11-14bk.pdf.

Krause, A., & Giansante, S. (2012). Interbank lending and the spread of bank failures: A network model of systemic risk. Journal of Economic Behaviour and Organization, 83, 583–608.

Lenzu, S., & Tedeschi, G. (2012). Systemic risk on different interbank network topologies. Physica A: Statistical Mechanics and Its Applications, 391(18), 4331–4341.

Nier, E., Yang, J., Yorulmazer, T., & Alentorn, A. (2007). Network models and financial stability. Journal of Economic Dynamics and Control 31(6), 2033–2060. http://www.bankofengland.co.uk/publications/workingpapers/wp346.pdf.

Sachs, A. (2014). Completeness, interconnectedness and distribution of interbank exposures: A parameterized analysis of the stability of financial networks. Quantitative Finance, 14(9), 1677–1692.

Tasca, P., & Battiston, S. (2014). Diversification and financial stability. London School of Economics, SRC Discussion Paper No. 10.

Teteryatnikova, M. (2014). Systemic risk in banking networks: Advanatages of “tiered” banking systems. Journal of Economic Dynamics and Control, 47, 186–210.

Upper, C. (2007). Using counterfactual simulations to assess the danger of contagion in interbank markets. BIS Working Papers 234.

Upper, C. (2011). Simulation methods to assess the danger of contagion in interbank markets. Journal of Financial Stability, 7(3), 111–125.

Watts, D. J. (2002). A simple model of global cascades on random networks. Proceedings of the National Academy of Sciences of the United States of America, 99(9), 5766–5771. http://www.jstor.org/stable/3058573.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

1.1 Determination of the adjusted connection probability \(p^{*}\)

While riskiness and the inhomogeneous distribution of the external assets can be implemented in a deterministic way, the introduction of the node property, connectivity, depends on a technical parameter, namely the adjusted connectivity probability, \(p^{*}\). In order to ensure a stable model evaluation, this parameter (which is only defined via an expected value) must be determined in a reliable way. An iterative numerical approach is implemented to determine \(p^{*}\): We start with an estimated value. The number of network links, Z, is calculated for up to 10.000 configurations generated for \(p^{*}\). Then, the average of the observed Z-values is interpreted as the expected value of the left-hand side of Eq. (10). These two steps are performed within a secant-like method to adjust \(p^{*}\) so that, finally, Eq. (10) approximately holds.

Table 4 shows our approximated values for the adjusted connection probability, \(p^{*}\), for different levels of \(\sigma _{p}^{2}\). Note that for the chosen model parameters, the targeted value for the expected number of links is 495. The small variations of \(p^{*}\) and Z indicate that \(p^{*}\) is determined with high accuracy, even if the variance \(\sigma _{p}^{2}\) exceeds the width of the reasonable interval, [0; 1].

Rights and permissions

About this article

Cite this article

Hübsch, A., Walther, U. The impact of network inhomogeneities on contagion and system stability. Ann Oper Res 254, 61–87 (2017). https://doi.org/10.1007/s10479-017-2401-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-017-2401-y